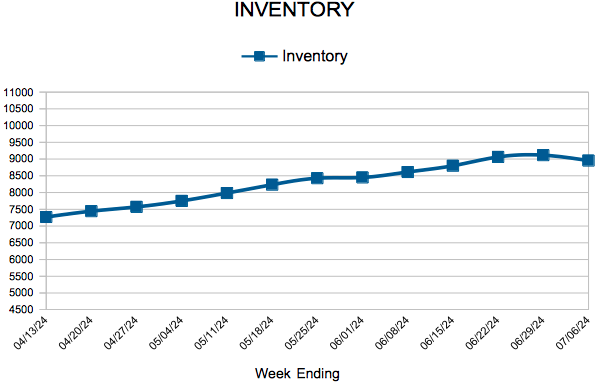

Inventory

612-558-1084

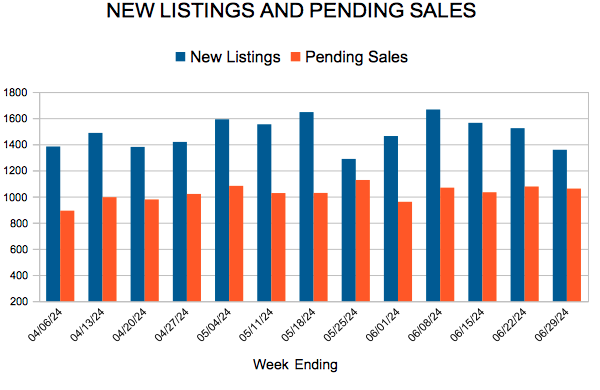

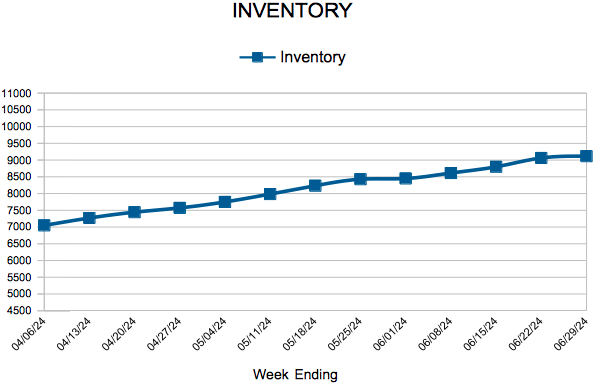

For Week Ending July 13, 2024

For Week Ending July 13, 2024

U.S. homeowners with a mortgage saw their equity increase 9.6% year-over-year in the first quarter of 2024, an average gain of $28,000 and the highest number since 2022, according to CoreLogic’s Homeowner Equity Insights report. At the state level, California saw the greatest equity gain at an average of $64,000 annually, followed by Massachusetts and New Jersey, at $61,000 and $59,000, respectively.

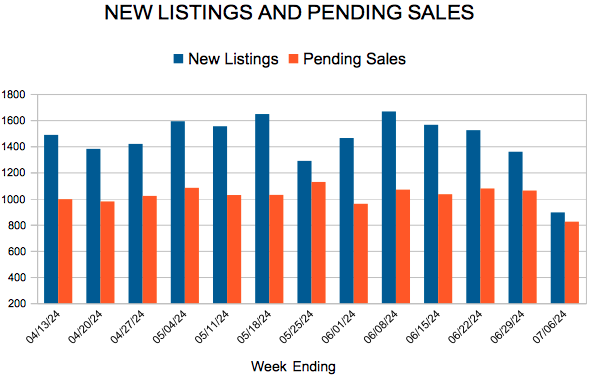

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING JULY 13:

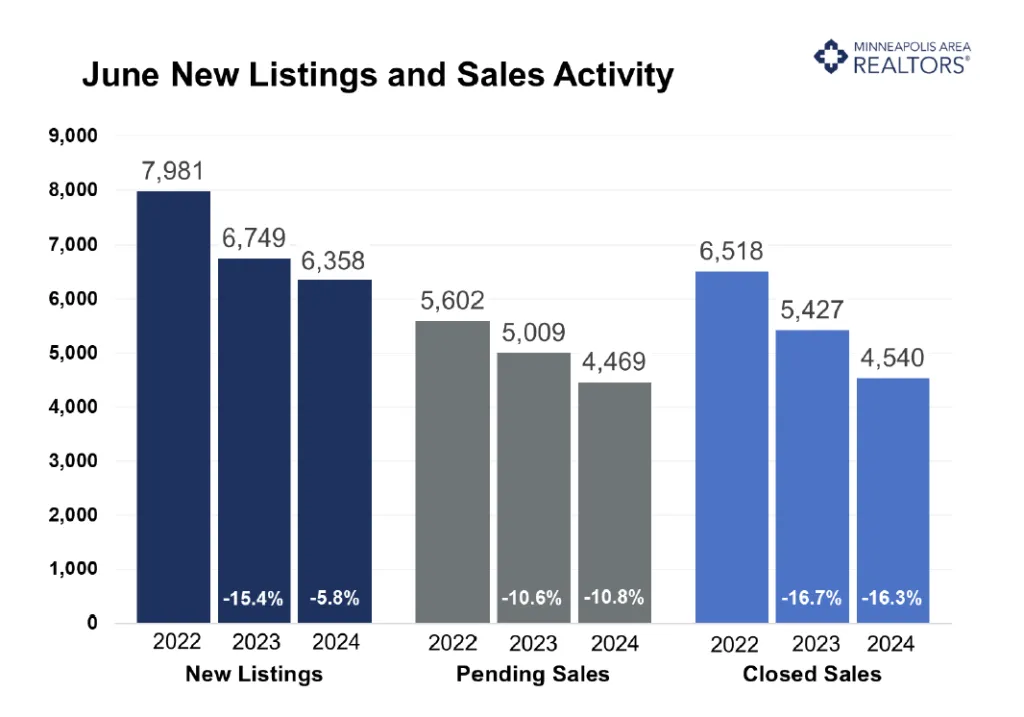

FOR THE MONTH OF JUNE:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

July 18, 2024

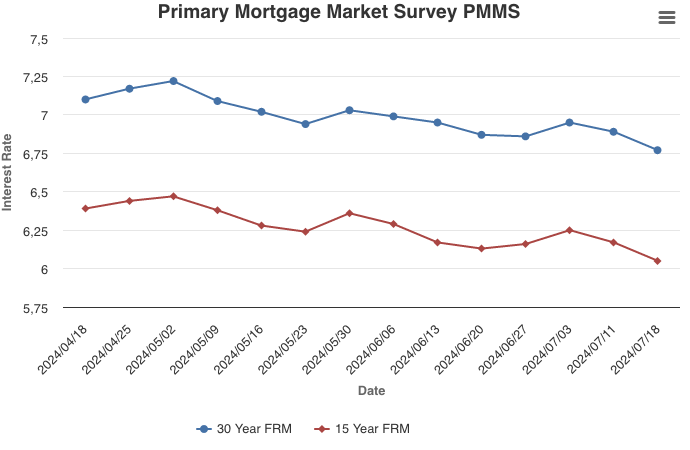

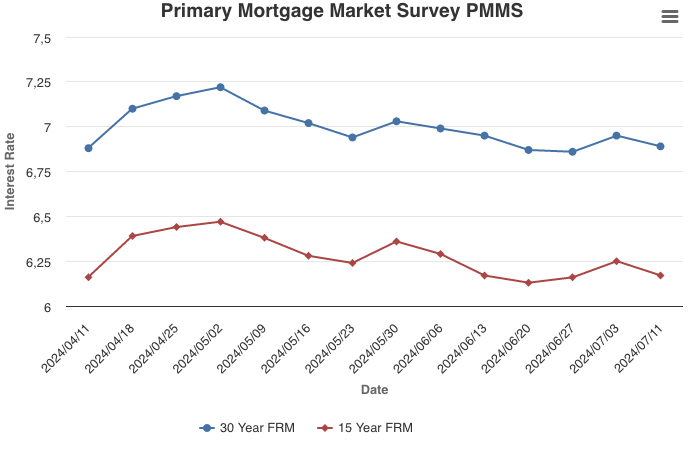

The 30-year fixed-rate mortgage fell to its lowest level since mid-March, dropping 12 basis points from last week. Mortgage rates are headed in the right direction and the economy remains resilient, two positive incremental signs for the housing market. However, homebuyers have yet to respond to lower rates, as purchase application demand is still roughly 5 percent below Spring, when rates were approximately the same. This is not uncommon: sometimes as rates decline, demand weakens, and the apparent paradox is driven by buyers making sure rates don’t decline further before they decide to purchase.

Information provided by Freddie Mac.

Metro home prices hit record high despite higher rates and more inventory

(Jul. 16, 2024) – According to new data from Minneapolis Area REALTORS® and the Saint Paul Area Association of REALTORS®, listings rose slightly compared to last year while sales softened. Inventory levels and prices were up.

Sellers, Buyers and Housing Supply

It’s official. Half of 2024 is in the books. That makes it a good time to zoom out and check on some year-to-date figures. So far this year, there have been 10.6% more new listings and 1.8% more pending sales metro-wide compared to the same period last year. That means seller activity has risen more than five times the pace of buyer activity on a year-to-date basis. Put another way, there was more supply coming online relative to demand—a trend confirmed by eight consecutive months of inventory growth. For June, the number of homes for sale was up 10.6% to 8,905 active listings. That’s the number of listings on which buyers can write offers. While buyers may be feeling less pressure with 850 additional homes to choose from, there are still only 2.4 months of supply, indicating a seller’s market; a balanced market is 4-6 months of inventory.

While this year has seen growth in both listings and sales compared to 2023, there seems to have been a cool-down in activity in May and June as signed purchase agreements dipped. At around 7.0%, mortgage rates in May and June of this year hovered higher than last year. And buyers are still feeling the triple punch of rising prices, low inventory and higher interest rates. There is a good amount of pent-up buyer and seller activity waiting in the wings for an improved affordability picture.

But all situations are unique. For example, move-up buyers with built up equity from their first home can roll that equity into their next property, while most first-time buyers don’t have that luxury. Additionally, market inventory and high interest rates lead to a decrease in overall activity, especially when it comes to more affordable homes as those buyers are the most rate sensitive.

Prices, Market Times and Negotiations

Listings in some areas are still getting multiple offers and selling for over list price. In fact, overall, sellers accepted offers at 100.1% of their list price on average. While perhaps surprisingly strong, that was down from last year. And those offers came in after an average of 34 days on market, which was up from last year. Single family homes specifically are selling after 31 days but condos are taking 56 days. “This is still a somewhat fragmented market where activity truly varies from price point to price point and area to area,” said Jamar Hardy, President of Minneapolis Area REALTORS®. “While we’re encouraged by more supply, the lack of affordability caused by higher mortgage rates and rising prices are still significant hurdles.”

The median home price was up 1.8% to $390,000. That was the smallest gain since December. The single-family median price rose to $425,000, while condos fell to just under $200,000 and townhomes dipped to $310,000. New home prices are just over $500,000 while existing home prices are $380,000. Low inventory and the mix of product selling—i.e. more luxury and new construction—are partly what’s keeping prices so firm. “We are observing that the limited inventory is still affecting prices and activity for more affordable properties,” said Amy Peterson, President of the Saint Paul Area Association of REALTORS®. “Partnering with a qualified and experienced professional will help consumers navigate the intricacies of this market.”

Location & Property Type

Market activity always varies by area, price point and property type. New home sales outperformed existing home sales while condo sales fell by over twice as much as single family. Sales over $500,000 performed better than sales under $500,000. Cities such as Mahtomedi, Hudson and North Oaks saw among the largest sales gains while Delano, Annandale and Elko New Market all had notably weaker demand. For cities with at least five sales, the highest priced areas were Deephaven, Shorewood, Tonka Bay and North Oaks while the most affordable areas were Hopkins, St. Paul Park and Spring Lake Park.

May 2024 Housing Takeaways (compared to a year ago)

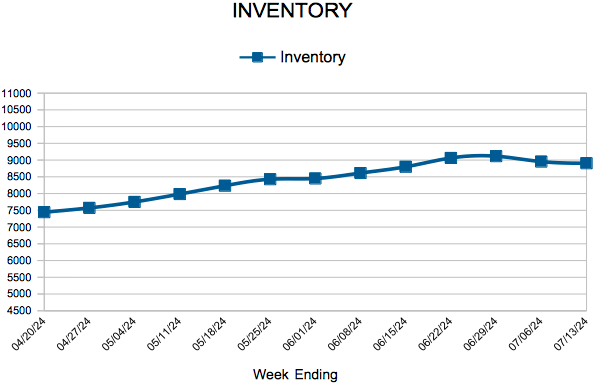

For Week Ending July 6, 2024

For Week Ending July 6, 2024

U.S. housing starts fell 5.5% month-over-month to a seasonally adjusted annual rate of 1,277,000, according to the U.S. Census Bureau. Privately-owned housing completions also declined, dropping 8.4% from the previous month to a seasonally adjusted annual rate of 1,514,000, as higher interest rates and ongoing labor and supply challenges continue to impact new home construction.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING JULY 6:

FOR THE MONTH OF JUNE:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

July 11, 2024

Following June’s jobs report, which showed a cooling labor market, the 10-year Treasury yield decreased this week and mortgage rates followed suit. There is also more inventory on the market, including a fair number of listings with price cuts, which is an encouraging sign for prospective buyers.

Information provided by Freddie Mac.